Monthly Market Roundup: August 2024

Disclaimer: Author holds ETH, SOL & JTO and may have intra-day/week positions and/or airdrop allocations in other coins mentioned in the article. Views and opinions are that of the author alone and do not represent the views or opinions of Etherscan. None of this is financial advice. Always do your own research before aping.

Note: We launched “The Spread”, our new trader-focused monthly newsletter! Read our announcement here.

Bitcoin & the Broader Market

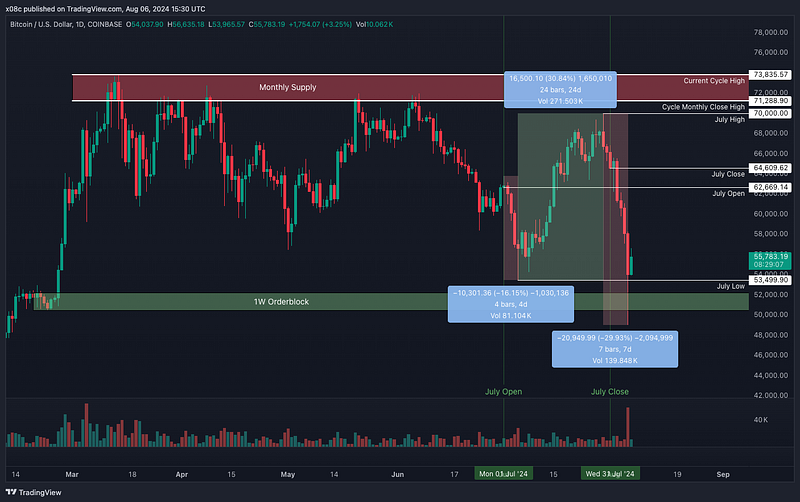

The past 5 weeks of price action have been a continuation of the viciously choppy downtrend in Bitcoin that began in March. This period can be split into three distinctive impulses highlighted on the chart below in blue:

Impulse 1: Swift -16% move in the first 4 days of July to a low of $53.5k, likely fueled by the aggressive climax of the German Government selling the last of their seized 50k Bitcoin forming the lows of the month.

Impulse 2: Failure to break down below May’s low followed by a +31% gradual 24 day climb to a multi month lower high at $70k.

Uptrend buoyed by positive sentiment around the German Government running out of coins on the 13th and anticipation of Trump speaking at the Bitcoin 2024 conference on the 27th, during which he endorsed a proposal by Senator Lummis for the US to hold up to 1M BTC as a strategic reserve asset, also stating that he’d stop the US selling seized BTC.

Topping of the uptrend coincided with Biden’s announcement that he would not stand for re-election, resulting in Harris emerging as nominee for the anti-crypto democratic establishment, in turn causing Polymarket odds of Trump winning to slump from highs of 70% to 53%.

Announcement of distributions to Mt.Gox creditors by Kraken and Bitstamp also took place towards the end of July.

Impulse 3: Devastating -30% move in the 7 days from July 29th to new lows briefly below $50k in a capitulation wick before closing at $54k to reclaim July’s low. This move resulted in over $2.7bn in liquidations across all asset pairs, with $800m of longs being liquidated on the August 5th selling climax alone. Likewise, aggregate BTC futures Open Interest fell a massive 29% from 37.4bn to 26.6bn over the period.

A fine example of the “stairs up, elevator down” a.k.a. “Inverse Dalai Lama” pattern, this impulse was likely driven primarily by the broader macro selloff caused by:

- Unwinding of the Yen ‘carry trade’ triggered by the Bank of Japan raising interest rates to 0.25%, its highest level since 2008.

- US recession fears intensifying due to worse-than-expected jobs data reported on August 2nd.

- Heightened Middle East war fears due to a report that US Secretary of State Tony Blinken had expressed concern to G7 counterparts regarding an imminent attack on Israel by Iran and Hezbollah.

However, it is worth noting that:

- This impulse began when the US government moved 29.8k BTC 2 days after Trump’s speech at Bitcoin 2024. Coinbase had announced a deal with the US Marshall Service to provide custody and trading services earlier in the month, so whether this transfer was done for custody or liquidation purposes remains unclear.

- On 30th July, Mt.Gox distributed an additional 34k BTC.

- On August 2nd, Genesis moved 16.6k BTC and 166.3k ETH, likely for in-kind distribution to creditors.

ETF Flows

July saw Bitcoin Spot ETF net inflows totalling $3.169bn, the third highest month since inception, up from $667bn in June. There were only 4 days of net outflows, with the highest being -$78m on 23rd July — the first trading day after Biden’s withdrawal announcement. August however, has already seen -$504m in net outflows over 4 trading days. As with previous months, the periods of weak flows coincided with downturns while strong flows accompanied uptrends.

Outlook

Reviewing the headwinds highlighted in last month’s issue, we see that 2 of the 4 have been removed. Namely, the distribution of Mt.Gox BTC to creditors and German Government selling. However, we still have the potential supply overhang from the US government’s 214k BTC (or 184k BTC assuming the 30k BTC moved last week was sold).

Likewise, miners are still struggling with profitability post-halving. As shown in the chart below by Capriole, production price has been very close to miner price (calculated as BTC price + (1D tx fees/ # 1D BTC mined) since the end of April. Currently, production price is 11% higher, meaning miners are losing 11c for every $1 spent.

From a technical analysis perspective, immediate supports are at $53.5k July low and then the 1W orderblock between $50.5–52.3k. To the upside, there are many clusters of resistances formed by this year’s swing lows, however we can take $60k as the most confluent level before July open above at $62.7k.

Tailwinds narratives discussed in the previous issue have also developed, albeit negatively. The reduction in expectations of a Trump winning the presidential race have dampened bullishness somewhat as it increases the likelihood of a prohibitive regulatory environment in the US persisting.

Likewise, sentiment around potential Fed rate cuts has somewhat deteriorated due to fears of a hard landing, whereby cuts are coming too late to prevent economic contraction into 2025. This also brings fears that the Fed will need to cut rates too rapidly now, which could induce a rebound in inflation.

On a more positive note, the Bank of Japan has quelled uncertainty around further near-term rate hikes.

Ethereum

ETH continues to underperform BTC to the upside, as seen in impulse 2, while also overperforming BTC to the downside, as seen in impulses 1 and 3. The last of these impulses brought price to a new yearly low at $2,131. XRP is the only other top 10 coin by marketcap to have swept it’s yearly lows.

While ETH has found support above the next weekly orderblock ($2,260 — $2,450) support below the previous 5 month trading range, price is still ~13% ($2,830) away from July low, confirming bullish macro market structure to be convincingly broken. To convincingly reclaim bullish market structure, we need to see high timeframe closes above the Q2 lows in the mid-high $2800's.

ETF Flows

The highly anticipated ETH Spot ETFs began trading on 23rd July, coinciding with monthly highs. The debut has been the highest net inflow day to date at $106.6m. Flows for the rest of the month were poor, closing July with net outflows of -$483.6m. The first 4 trading days of August have seen a marginal improvement, with net inflows of $119.6m, reducing net outflows since inception to -$364m. For comparison, BTC Spot ETFs saw net inflows of $759.6m in the first 11 days of Trading. A silver lining perhaps is that ETHE — the main source of outflows — has now sold 2,203 of the 9,200 seeded ETH.

Outlook

Reviewing the bullish and bearish arguments from last month’s issue, we can conclude that Rewkang’s thesis regarding a lack demand for ETH ETF products is being proven correct so far as inflows have been unable to match outflows from Grayscale’s ETHE. Bitcoin overcame similar heavy initial outflow pressures from Grayscale’s GBTC fund with strong inflows — particularly from Blackrock and Fidelity.

Likewise, L2 (farming) fatigue continues with ZKSync and Blast tokens debuting at $6bn and $3bn FDV respectively, a far cry from the 10 figure FDV debut of Starknet earlier in the year. Prices of both are down ~70% since launch.

Taking a look at the ETH/BTC ratio chart, it becomes very difficult to rationalize being long ETH instead of BTC, especially on a risk-adjusted basis. The multiyear downtrend of lower lows and lower highs continues with price touching 0.04, a level not seen since May 2021.

On the bullish side, there have been some interesting takes regarding Ethereum ecosystem protocols with product-market fit and strong revenue streams. For example, Pantera Capital published a report sharing the perspective that based on historical data, we are entering a new phase of the bull market where bitcoin dominance begins to trend down, with the major beneficiary being “tokens with sound fundamentals”. A possible explanation for this is the wealth effect, where bitcoin holders diversify to riskier assets to chase higher returns.

Another thesis worth exploring is Taiki Maeda’ AAVE redemption arc, based on the approval of a fee switch which would see value accrue to tokenholders beyond their existing governance rights.

Solana

SOL is the only major that did not break down from its 2024 range, while already being in the process of a July Open reclaim attempt — something BTC and ETH are ~15% and ~40% away from respectively. While it overperformed BTC to the downside by ~30% in impulses 1 and 3 this month, it overperformed to the upside by 100%.

July Open-Close range of $146-$172 would appear the immediate levels of support and resistance respectively.

Meanwhile, we also have a blue-sky breakout above all-time-highs for the SOL/ETH ratio. With ETH at 300bn market cap and SOL at 70bn, the path of least resistance would appear to be trend continuation.

Closing thoughts

“There are decades where nothing happens; and there are weeks where decades happen.” — Lenin

The market has had an overwhelming amount of information to process during this period, from governments selling and bankruptcy distributions, to gray swan geopolitical and macroeconomic events.

It likely takes time for the market to digest all this on top of multi-month technical range breaks, so be patient and move slowly. As Cred would say, do your business at range extremes, don’t diddle in the middle.

Periods like these are never easy, conditions are perilous and cruel.If you feel like you need to take a break from the markets, you absolutely should. If there is a time for leverage, this isn’t it. Come back stronger, fighting fit.